The Departments of Health and Human Services, Labor, and the Treasury, as well as the Office of Personnel Management (Departments) recently finalized the Independent Dispute Resolution (IDR) Operations rule under the No Surprises Act (NSA). Although many self-funded group health plan fiduciaries won’t have to deal directly with the operational changes to the federal IDR process, the broader implications for employer sponsored group health plans are significant and deserve close attention.

Background

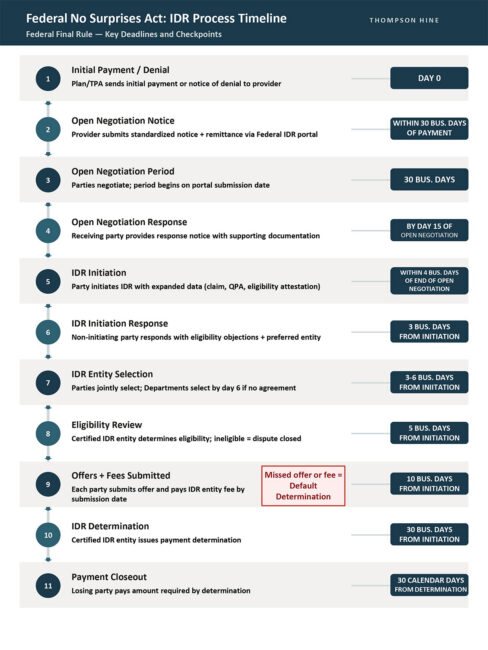

The NSA, first effective in 2022, established a federal IDR process to resolve payment disputes between out-of-network providers and health plans for surprise medical bills. Congress expected the system would be used relatively infrequently, with the Departments estimating approximately 17,333 disputes per year. However, actual utilization far exceeds those expectations: from mid-2022 through the end of 2025, approximately 4.8 million total disputes have been filed.

The final rule focuses on how the federal IDR process works in practice, addressing the mechanics of IDR, including payer disclosures, remittance codes, open negotiation, IDR initiation, eligibility review, batching, bundled payment arrangements, fee collection, and the federal IDR portal. The final rule is effective August 3, 2026, though the applicability dates for the different provisions vary.

Key Provisions of the Final Rule

Reduced Administrative Fee. The final rule lowers the federal IDR administrative fee to $15 per party per dispute, a significant reduction from previous administrative fee amounts. This new reduced fee is applicable beginning June 11, 2026. A lower fee may make the process more appealing for providers and further increase dispute volume, which could exacerbate the capacity problems that have plagued the system.

Payer Registration Requirement. The final rule creates a federal IDR registry for plans and issuers. Self-insured group health plans, FEHB carriers, and health insurance issuers must register with a new Federal IDR Registry within 90 business days of its availability (or by the date coverage subject to the federal IDR process begins, if later). Third-party administrators (TPAs) or other service providers may register on behalf of group health plans.

Open Negotiation Through the Federal Portal. Open negotiation will move to the federal IDR portal once functionality is available. Because the IDR process cannot be initiated before completion of the 30-business-day open negotiation period, this will allow the Departments and certified IDR entities, the independent third-party arbiters that resolve disputes in the federal IDR process, to more easily track eligibility of disputes. Plans and issuers cannot require providers to use proprietary payer portals instead of the federal IDR portal for open negotiation notices. The final rule requires that the responding party, usually the payer, submit an open negotiation response notice by the 15th business day after the initiating party submits an open negotiation notice to the portal).

Formal Initiation Response Requirements. If negotiations fail, either party may initiate the IDR process within 4 business days after the end of open negotiation. Under the new rule, the non-initiating party, usually the payer, must now provide a written response to the notice of IDR initiation within 3 business days after the date of IDR initiation, including an attestation as to the eligibility of the dispute or an explanation of why it is ineligible, with supporting documentation.

Eligibility Review Remains With IDR Entities. The Departments did not finalize the proposed eligibility review process under which they would have made eligibility determinations in certain extenuating circumstances. Instead, certified IDR entities will continue to decide whether parties are eligible for the IDR process. In addition, the final rule adds a 5-business-day timeline for eligibility determinations after final selection of the IDR entity.

Batching Revisions. The final rule increased the number of line items permitted to be considered jointly as part of a batched dispute from the proposed rule, from 25 to 50 line-items. In addition, providers will be able to batch claims based on single patient encounters and based on certain CPT code ranges. The cooling-off period, during which a party is unable to bring another claim against the same party for a similar item or service, will be shortened for batched disputes from 90 calendar days to 30 business days, allowing batched disputes to be filed more quickly following an IDR determination. This 90-day cooling off period will not be changed for non-batched disputes.

Bundling Definition. The Departments clearly distinguish bundling from batching in the final rule. The final rule provides a definition for bundling, under which a bundled payment arrangement is defined as an arrangement in which a single billing code covers multiple items or services provided to one patient.

New Disclosure and Remittance Code Requirements. Plans and issuers will be required to provide standardized claim adjustment reason codes (CARCs) and remittance advice remark codes (RARCs) with initial payment or denial communications for NSA-related claims. The intent of this new disclosure requirement is to help providers determine earlier whether a claim may be subject to the NSA, whether federal IDR may be available, and which plan or issuer is responsible. The Departments will provide additional guidance identifying the specific codes before payers are required to implement this requirement.

Thompson Hine Takeaways

Further Intervention is Needed to Curb Documented Abuses of the IDR Process

For employer group health plans, and particularly self-funded plans that ultimately bear the cost of claims, the IDR process has created serious and growing financial exposure. As we have previously written, providers prevail in roughly 88% of disputes, with median 2024 awards at approximately 450% of typical in-network rates. IDR administrative costs in the first half of 2025 alone totaled $844 million, and these costs flow directly to employer sponsored group health plans. A plan’s TPA/insurer likely handles these disputes, but may not proactively report on IDR volume, outcomes, or costs unless specifically asked.

Furthermore, while a key policy objective of the NSA was to shield participants from abusive and financially debilitating balance billing, it may instead be exacerbating the health care affordability crisis. If the NSA ultimately results in significantly inflated claims payments and plan administration costs, participants might share the burden of those inflated costs through increases in plan premiums and participant cost share obligations.

The Rule May Reduce the Number of Ineligible Disputes

Data shows that ineligible claims constitute approximately 20% of all closed IDR disputes, and plans challenged 40 percent of cases as ineligible in the first half of 2025. This includes disputes involving Medicare and Medicaid beneficiaries, claims that are categorically ineligible for the federal IDR process. Employer group health plans have also been impacted by ineligible claims filed within the cooling-off period. Plans must expend resources responding to these ineligible disputes, including paying non-refundable administrative fees, even when the disputes are ultimately dismissed.

The final rule may provide some relief here. Enhanced disclosure requirements (mandatory CARCs/RARCs, registration numbers, and eligibility information exchanged during open negotiation) should reduce ineligible filings by providing clearer front-end information. The payer registry should curb instances of disputes initiated against the wrong party, and the 3-business-day documented eligibility objection deadline creates a more robust screening mechanism.

Still, many of the changes under the final rule are dependent upon the parties acting in good faith. In recent litigation, a health insurer alleged that nearly 60 percent of more than 27,000 disputes initiated by a single provider group were ineligible for IDR. A complaint in another case describes the “intentional and knowing submission” of ineligible disputes in order to overwhelm the payers and the system. The regulatory changes may not prevent continued submission of ineligible claims in such circumstances, and the parties will be at the mercy of sometimes-overwhelmed IDR entities with limited recourse if they disagree with an IDR entity’s determination.

Fraudulent and Inflated Provider Demands

Recent litigation has exposed alarming patterns of alleged provider fraud, including fictitious billed charges, misrepresented qualifications, and abuse of the ex parte process. While the rule’s structured documentation requirements and portal-based submissions may deter low-quality filings, the final rule does not address inflated charges, impose consequences for provider misrepresentations, alter the opaque nature of proceedings, change how IDR entities select between offers, or give plans a mechanism to recover fees on fraudulently initiated disputes.

What Employer Group Health Plan Fiduciaries Should Do Now

Employer group health plan fiduciaries should continue to monitor IDR activity for their health plans and analyze reporting from their TPAs on IDR disputes involving the plan. Because of the significantly reduced administrative fee, fiduciaries should examine their TPA agreements and make sure the pricing is consistent with the lower amount. In addition, fiduciaries should prepare for the new registration requirement, working with their TPAs to ensure timely compliance once the registry becomes available. Now is a good time to review administrative agreements and confirm that TPAs are operationally ready to meet the final rule’s new disclosure, remittance code, and response obligations.

Please contact the authors or your Thompson Hine attorney with any questions.

For ease of viewing, the chart is available in full-size pdf format here.